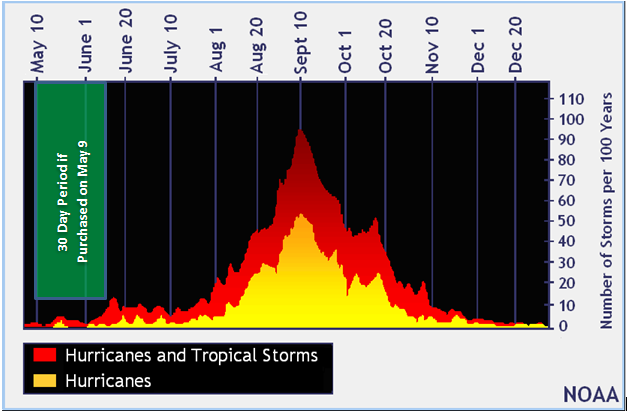

Many do not realize it takes 30 days for new policies to become effective, so with less than 30 days away from the 2018 Hurricane Season, there is still time to purchase flood insurance.

Flood Insurance is one of the most misunderstood items when it comes to insuring someone against flooding. If a property is not in a special flood hazard area many feel they are safe from flooding. Usually, after the the unthinkable happens, the first statements from many are “No one told me I could flood” or “I was told I did not need flood insurance.” The only partial truth about the later statement is that if you are not in a special flood hazard area there is no federal requirement to purchase flood insurance. This does not mean, however, you “do not need” flood insurance or that you will never flood.

In reality no one is completely safe from flooding, especially in the greater Houston area where the overall terrain (elevation) is extremely flat with streets designed to hold a specific volume of water during intense storm events. I emphasize “specific” because everything in this world has design limit. Eventually, thanks to Mother Nature, those limits can be exceeded. For instance, in the Greater Houston area the underground storm sewers and allowable street ponding, before flooding structures, are designed to handle between 10 to 13 inches of rainfall over a 24 hour period based on a certain amount of impervious cover. Depending on when your subdivision was built, the actual amount of impervious cover, and the actual duration and volume of rainfall, the system’s true capacity can vary.

Looking back at the 2016 Memorial Day Flood in Harris County an estimated 10,250 homes were flooded. Out of those, 3,740 were outside of the 1% Annual Chance Special Flood Hazard Area (100-Year Floodplain, or Zone A/AE) which makes up about 36% of the homes flooded.

It only takes a couple of inches of water to cause over $10,000 in damages to both your home and contents. And remember, it is not just naturally rising water that can cause damage to your home. Emergency and/or personal vehicles driving through ponding water in the streets can create shallow waves that can enter your home through doors and weep holes. Also, homes built on pier and beam foundations can have water that sits underneath the structure, that can be absorbed through the bottom side of wood decking, damaging the substructure, flooring and, depending on the duration of flood, the lower sections of walls. Flood insurance is such a small price to pay to cover such a devastating event, especially if you live outside of a special flood hazard area.

If purchased on May 9, your policy would not be effective until after the start of Hurricane Season; however, that is still plenty of time before the peak of the season.

Here are some quick facts about flood insurance from FloodSmart.Gov:

- FACT: Homeowners and renters insurance does not typically cover flood damage.

- FACT: More than 20 percent of flood claims come from properties outside high-risk flood zones.

- FACT: Flood insurance can pay regardless of whether or not there is a Presidential Disaster Declaration.

- FACT: Most federal disaster assistance comes in the form of low-interest disaster loans from the U.S. Small Business Administration (SBA) and you have to pay them back. FEMA offers disaster grants that don’t need to be paid back, but this amount is often much less than what is needed to recover. A claim against your flood insurance policy could, and often does, provide more funds for recovery than those you could qualify for from FEMA or the SBA — and you don’t have to pay it back.

Visit https://www.floodsmart.gov/faqs for more Q&A about Flood Insurance.

Flood Insurance Resources

FloodSmart.Gov: First, Prepare for Flooding

FloodSmart.Gov: Lowering your Premium Cost (And Risk)

FLASH Insurance Guide: If Disaster Strikes, Will you be covered?

FEMA How Do I Buy Flood Insurance?

Texas Department of Insurance: Flood Insurance, 4 Things to Know